3 ways to help your merchants with stablecoin payouts

With $7tn in stablecoins settled on blockchains in 2023, some of your merchants may already be interacting with them, especially if they do business in Latin America, South East Asia or Africa where stablecoin adoption is strong.

As a fintech product leader, how can you support them?

At BVNK, we process $6bn+ in payments each year on behalf of fintechs and global businesses – most of them involve a stablecoin. In this post, I’ll cover 3 ways to help your merchants with stablecoin payouts, as well as key considerations for how to deliver the functionality.

But first a note on the global adoption of stablecoins.

Are people using stablecoins for payments?

Stablecoins were designed to bring stability and predictability to the crypto ecosystem, addressing a major drawback of other cryptocurrencies like bitcoin: high volatility. In the last decade, stablecoins have found other important uses: as a store of value in countries with volatile currencies, and as a way to send payments across borders in an instant. Though today they make up only a fraction of the global financial system, they’re fast becoming a popular way to transfer value globally at speed, with major players like Visa, PayPal and Stripe all investing in stablecoin technology.

Stablecoin adoption isn’t yet spread evenly across the globe but there is heavy adoption in the world’s fastest-growing economies. If your supplier or customer is based in Latin America for example, there’s a 1 in 3 chance that they will have already used stablecoins to pay for something, according to this Mastercard study.

Now let’s look at 3 ways that fintech product leaders are using stablecoins to pay out globally in minutes, not days.

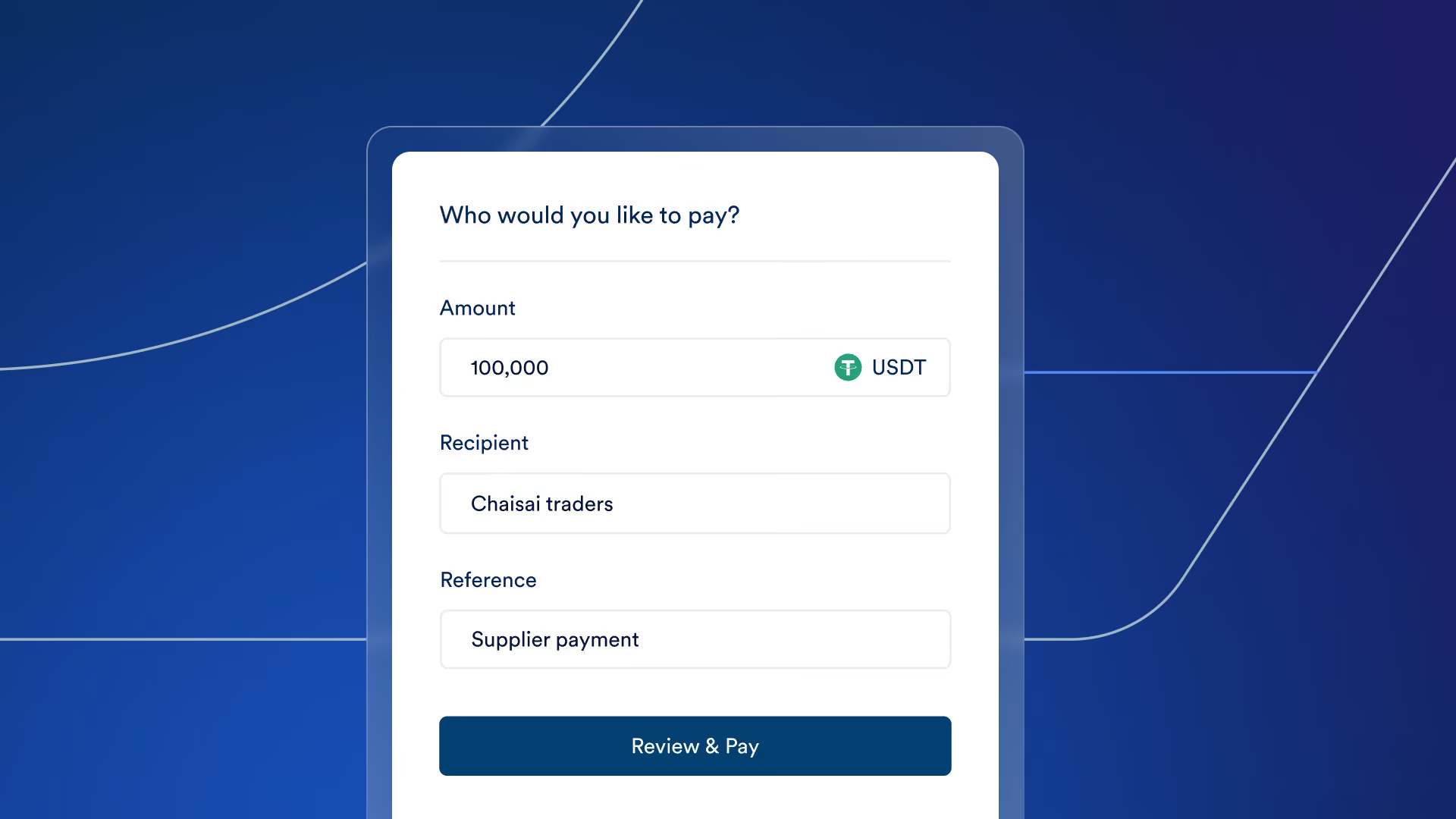

1. Settling your merchants

Fintechs move money every day for their merchants – how fast and reliably you can do so creates competitive advantage. The real-time nature of stablecoins gives payment providers an edge, offering faster settlement than Swift for many cross-border routes and reducing the need for you to hold capital in prefunded accounts. Some of the world’s biggest payment companies are already testing stablecoin settlement, including Visa, Worldpay and Nuvei.

Old way:

Fintech collects payments on behalf of its customers in local markets, converts to euros, dollars or pounds and sends to merchants via Swift. Funds take 2-5 days to settle.

New way:

Fintech converts fiat to stablecoins, and sends funds to the stablecoin wallet of their international merchant in minutes.

2. Consumer payouts

Let’s imagine a fintech company that helps businesses to pay out to consumers globally, including refunds, withdrawals and winnings. Fintechs like Worldpay are exploring how they can enable payouts to stablecoin wallets in markets where stablecoin adoption is high and traditional payment options may be slow and less reliable.

Old way:

Fintech enables payouts to payment cards, bank accounts, digital wallets or mobile money apps to meet demand from consumers.

New way:

Fintech enables payouts to stablecoin wallets as an additional option for markets where there is demand to hold digital dollars (eg to avoid local currency volatility). Stablecoin payouts settle in minutes and often for lower transaction fees.

3. Salary payouts

The third use case we see is payroll. Specifically: paying contractors and gig workers, including software developers, creators and consultants in emerging markets – where demand for digital dollars is high.

While there are challenges in managing ‘pay as you earn’ tax using stablecoin payments, so far stablecoins have mainly been used to pay self-employed individuals (e.g. consultants, contractors), who are typically responsible for paying their own taxes. According to fintech Deel, 4% of its global contract workforce took payment in crypto in 2022. Let’s look at an example:

Old way:

Fintech enables payroll for international workers on behalf of its customer, but it can take up to a week for those workers to get their money, and they may lose value to unfavourable currency conversion if their local domestic currency has become weaker against the dollar for example.

New way:

Fintech facilitates payroll in stablecoins for global contractors. Contractors opt to take a portion of their salary in stablecoins, getting paid instantly in digital dollars (and at less cost to the business paying them – up to 10x savings on foreign exchange fees for some emerging market routes).

Build or partner? Considerations for product teams

Fintechs are no strangers to innovation, but stablecoins present a new challenge. The technical and compliance demands they place on product and operational teams are significant, especially if those teams have honed their craft in the fiat world.

So, should you build the capability from scratch or partner with a provider like BVNK?

Like most build or buy decisions, that really depends on what’s most important to you. Do you want to reduce upfront costs, or minimise revenue share fees? Costs for building your own payments platform for example can be anywhere from $250,000 to $1 million, depending on your requirements. Do you need to go to market fast, or do you have the time and capacity to build?

There are also other important considerations more specific to enabling stablecoin payouts, These include:

- Coverage: Do you want to enable multiple stablecoins (eg USDC, USDT, PYUSD) across multiple blockchains (Tron, Etherum, Polygon and Binance Smartchain )? Options here include working directly with each issuer separately or partnering with a provider like BVNK to gain access to multiple stablecoins in one API.

- Blockchain knowhow: How much blockchain knowledge is there in your organisation: to what extent can you run your own blockchain nodes, and implement and run integrations with different blockchains? This can influence how much you need to rely on a partner.

- Functionality: managing wallets, gas fees

Do you want to offer full stablecoin wallets to your merchants or simply facilitate payouts for them? Do you want to manage the backend routing of stablecoin funds, reconciliation, payment references and gas fees, or do you prefer to use a partner? - Custody and security: Is it important for you to be able to fully or partially custody private keys for stablecoins, and do you need to store merchant data on your own servers, or are you comfortable to outsource this?

- Compliance: Do you have the appetite to manage compliance for stablecoins, eg scaling the team, implementing digital asset transaction monitoring, managing global regulatory horizon scanning? Do you have the appetite to obtain the right licensing for the markets where you want to use stablecoins?

Answering these questions can give you a steer on the right approach for your business.

.avif)

Flexibility across payment rails is key

Stablecoins offer a new way to move money globally at internet speed. But to benefit from stablecoin payments today, flexibility is critical. As a fintech, you need the ability to move between fiat and stablecoin payment rails according to the demand you see from customers, as well as your own preferences for managing risk and cost.

BVNK partners with many fintechs to give them access to stablecoins and fiat payments infrastructure in a way that works for them. Learn more

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

Never miss an insight.