Build your stablecoin strategy

1. Introduction

Your users want to send and receive money instantly across borders. Stablecoin technology makes this possible. Research from YouGov and BVNK shows 77% of stablecoin users would open a wallet with their primary fintech or banking app if offered one, they just need it to feel native.

Businesses are already using stablecoin infrastructure for payment workflows. On our platform, embedded stablecoin wallet volume grew 263x year on year. PSP and fintech customers now account for 75% of that volume (up from 58% twelve months ago), signaling that stablecoins have moved from crypto-native experimentation into mainstream enterprise use.

Our data also shows a shift toward 24/7 financial access. Half of all stablecoin transactions on our platform happen outside banking hours – reflecting demand for always-on payment infrastructure.

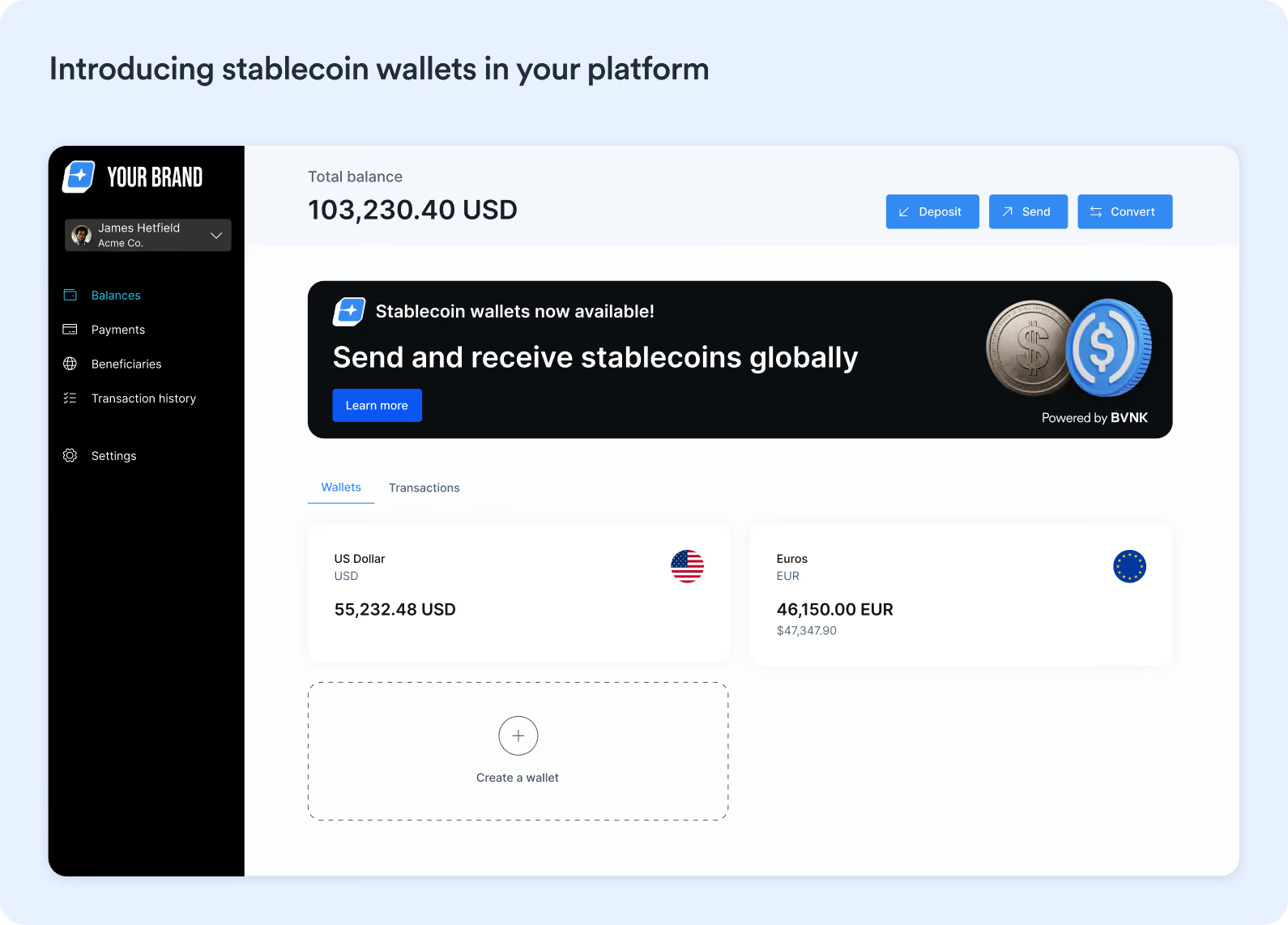

For fintechs and enterprise, the stablecoin wallet is becoming the center of gravity for how businesses move money. It's the interface where send, receive, convert, spend and earn happen from one place. One integration connects stablecoins, fiat currencies, and payment rails globally.

But launching stablecoin capabilities used to mean months-long delays, fragmented compliance frameworks, and vendor complexity. That's no longer necessary. This guide documents what we're seeing across enterprise deployments – how teams are moving faster, what embedded wallet models look like, and what matters when building your strategy.

For product or compliance leaders exploring stablecoin wallets, this guide covers:

- Use cases:Real-world examples (B2B payments, payroll, remittances), fund flows and interactive demos.

- Where to launch:Global market signals and adoption metrics.

- How it works:Setup, responsibilities, compliance – what you control vs. your provider.

- Product capabilities:Features, onboarding and service levels.

- Building your experience: Design and rollout guidance.

- Pricing:Fee structures demystified and a guide to pricing your stablecoin service.

If you want to dig deeper, our team is running a live Stablecoin wallets 101 session on August 13. We'll cover the fundamentals and discuss practical considerations for teams evaluating stablecoin wallets. Register below.

2. Explore use cases: what can you build?

Embedded stablecoin wallets enable businesses to send, receive, store, convert, spend and earn stablecoins. The most common use cases we see are:

- B2B payments: Send and receive payments cross-border with suppliers, merchants and partners, or your own entities.

- Salary and gig payouts: Enable international workers, sellers and creators to receive wages or earnings in stablecoins.

- P2P remittances:Faciliate peer to peer international transfers that end in stablecoins, are funded in stablecoins or use stablecoins to accelerate the middle of a transaction.

- Global digital dollar accounts: Give your customers a global dollar account backed by stablecoins for saving, spending, earning, or making payments.

Read on to learn about these, see what market leaders are building, and test drive solutions with our interactive API demos for B2B payments, Salary payouts and Global digital dollar accounts.

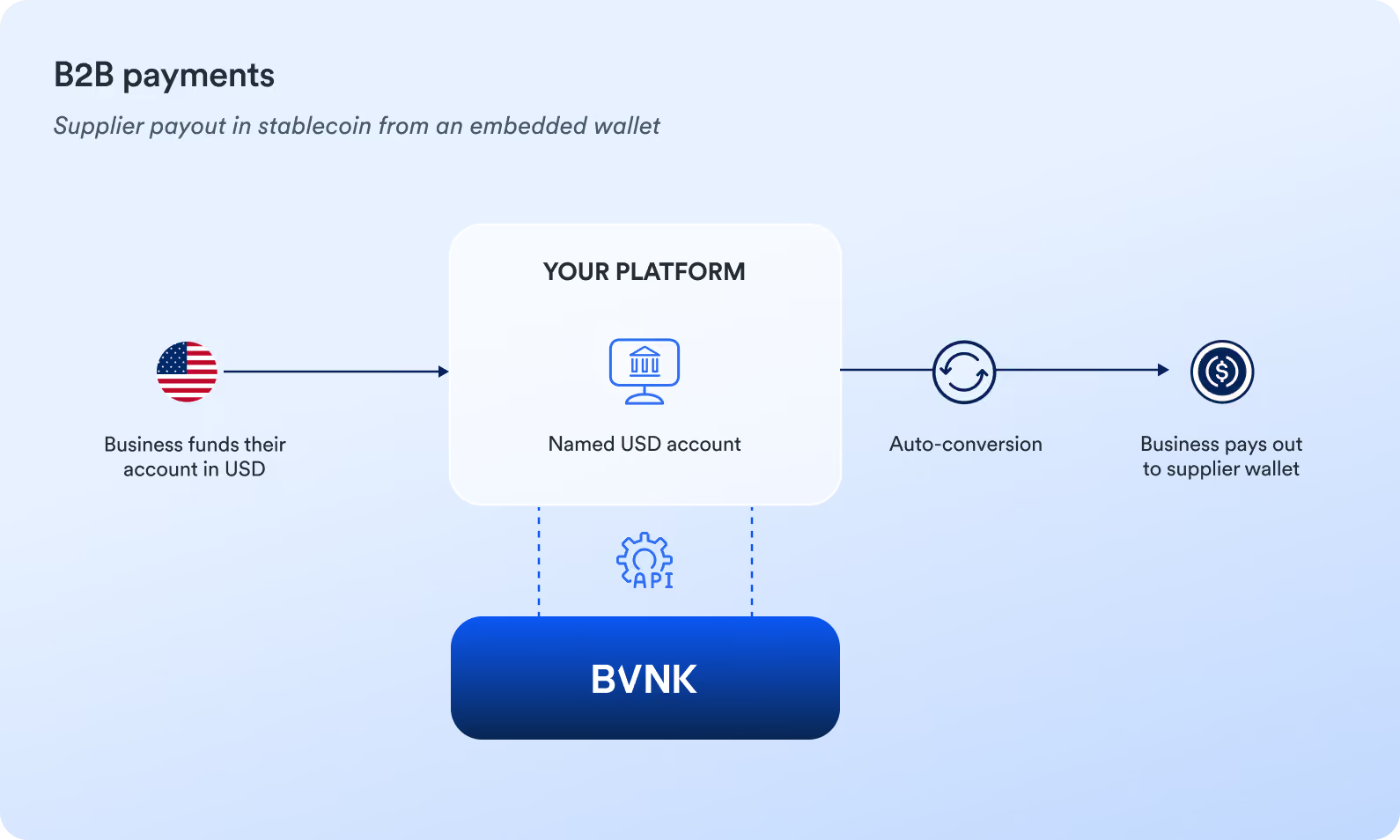

B2B payments

Businesses can send and receive payments cross-border with suppliers, merchants, partners, or their own entities using embedded wallets.

How it works – hold USD:

Your customer wants to hold USD but pay out to their suppliers in stablecoins.

- Fund:You or your customer fund a named wallet in USD/GBP/EUR in your platform (powered by BVNK).

- Initiate:Your customer selects to pay out in stablecoins in your platform.

- Send:BVNK automatically converts the fiat currency to stablecoins and sends to the supplier's wallet address.

How it works – hold stablecoins:

Your customer wants to hold stablecoin balances and pay out to their suppliers in stablecoins.

- Open:Your customer opens stablecoin wallet in your platform.

- Fund:Your customer moves funds from their fiat wallet to their newly open stablecoin wallet.

- Convert:BVNK converts the funds from fiat to stablecoin.

- Send/receive:Your customer sends stablecoin payouts to the receiver, BVNK ensures payout lands in the receivers wallet.

Challenge:

Corpay serves more than 800,000 clients worldwide, processing over $12 billion in corporate payments and $26 billion in foreign exchange each month across 145+ currencies. At this scale, moving liquidity quickly and reliably across borders is critical – yet traditional banking infrastructure operates on fixed hours and fixed rails, creating delays and inefficiencies. Corpay customers need flexible payment options that work beyond banking hours, with better capital efficiency and faster settlement for global transactions.

Solution:

Corpay partnered with BVNK to integrate stablecoin wallets and settlement capabilities into its platform. The integration enables Corpay's customers to hold stablecoin balances alongside fiat balances, with embedded wallets for sending, receiving, storing, and converting stablecoins directly within the platform. This gives customers access to always-on payment rails that operate 24/7.

Corpay is also integrating stablecoin settlement into its own treasury operations. This reduces reliance on pre-funded accounts, improves capital efficiency, and enables faster movement of funds across its global footprint outside of its proprietary network.

Result:

- 24/7 settlement capability enabling customers to move funds beyond traditional banking hours.

- Improved capital efficiency for Corpay through reduced pre-funding requirements and faster liquidity movement.

- Faster cross-border transactions leveraging stabelcoins for settlement in minutes.

Demo: B2B payments

Create an instant personalized demo to see how stablecoin wallets could work in your platform.

Salary and gig payouts

International workers, sellers and creators can receive wages or earnings in stablecoins using embedded wallets.

How it works

A contractor wants to receive a salary in stablecoins.

- Fund:You fund a named wallet in USD in your platform (powered by BVNK).

- Initiate: Contractor selects to withdraw salary in stablecoins. They create a stablecoin wallet and select stablecoins as payout method. They then select the amount and confirm withdrawal.

- Send:BVNK automatically converts the fiat currency to stablecoins and updates the user’s USD and stablecoin wallet balance, or if user opts to receive to an external wallet – BVNK processes payment.

Challenge:

The global freelance workforce is thriving, growing 15x faster than traditional jobs, while the global gig economy market is expected to triple in size by 2032. And with the rise of global HR services and employer of record platforms like Deel – it's easier than ever for businesses to hire and manage freelance talent globally.

Despite this, paying workers overseas remains a challenge. Today's cross-border payment systems can leave workers waiting days for money – only to lose out to unfavourable currency conversions at the last mile. Employers meanwhile can be held back by tied-up capital and exposed to foreign exchange risk.

Solution:In Spring 2024, Deel teamed up with BVNK to enable embedded stablecoin payouts to global contractors. With BVNK's infrastructure, workers employed via Deel can fast-track wage payments with dollar-backed stablecoins like USDC, receiving them in minutes not days.

With BVNK's auto-conversion capabilities, there's no need for the Deel team to handle crypto. They fund their BVNK account in USD, EUR or GBP, and funds are converted automatically on payout. With this solution in place, Deel can ensure a seamless service for contractors, while remaining at the forefront of global payments innovation.

Following strong contractor adoption, Deel expanded the partnership in 2026 to stablecoin salary payouts for full-time employee. Employees opt in once, stablecoins land on payday, while companies can also fund payroll accounts in stablecoins directly.

Result:

- Settlement reduced from 3-5 days to near-instant.

- 10,000+ contractors in 100+ markets now have opted to be paid in stablecoins.

- Full-time employee stablecoin payroll expanding use case from gig economy to enterprise global payroll.now live,

Demo: Salary and gig payouts

Create an instant personalized demo to see how stablecoin wallets could work in your platform.

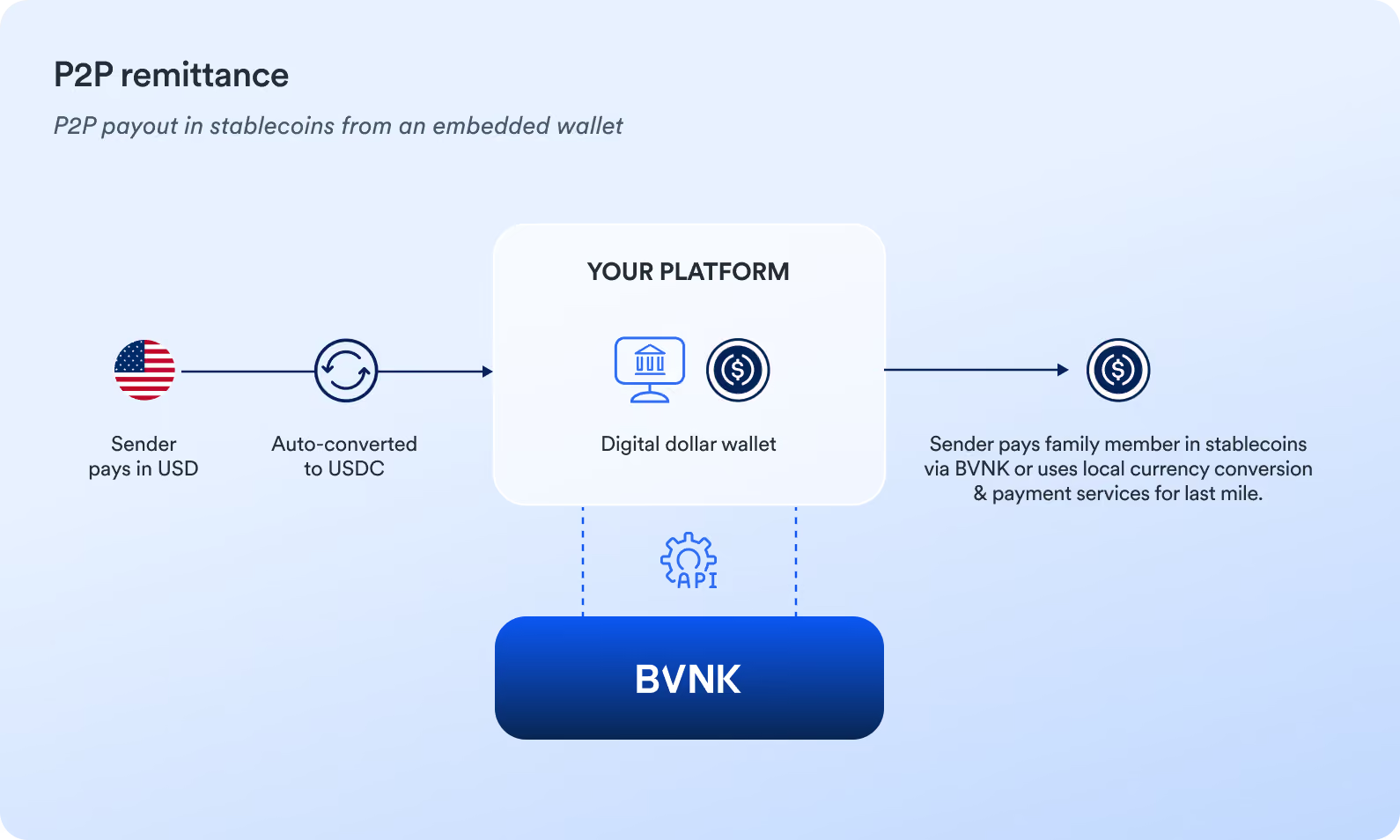

P2P remittances

Customers can send international transfers via stablecoins to family and friends – either ending in stablecoins, funding in stablecoins, or using stablecoins to accelerate the middle of a transaction.

How it works:

Your user in the USA wants to send money to a family member in Mexico.

- Sign-up:Your customer opens a USDC digital dollar wallet in your app.

- Fund:You or your customer fund the named wallet in USD in your platform (powered by BVNK). BVNK converts USD to USDC credits your customer’s balance.

- Initiate:Your customer adds beneficiary details and sets up/confirms stablecoin payout from your platform.

- Send:BVNK sends USDC to beneficiary wallet.

Global digital dollar accounts

Customers can hold a global dollar account backed by stablecoins for saving, spending, earning, or making payments.

How it works:

Your user pays in USD to a digital dollar account for global spending, saving and earning.

- Sign-up:Your customer opens a USDC digital dollar wallet in your app, powered by BVNK.

- Fund: Your deposits USD into the wallet. BVNK converts USD to USDC credits your customer’s balance.

- Send: Your customer sends USDC to a beneficiary wallet.

- Earn:Your customer can hold stablecoins in their wallet and earn rewards on idle funds.

Challenge:

Remote workers in emerging markets like Latin America and India face significant obstacles when receiving payments from US employers including settlmeent delays of 3-5 day, unfavorable currency conversion rates and limited banking options in local markets. Utoppia customers want access to US dollars, but also need to spend and move those funds globally without friction.

Solution:

Utoppia, a US-based fintech founded to give remote workers in emerging markets access to US dollar banking services, integrated BVNK's stablecoin infrastructure to solve this problem. Utoppia users receive US dollar payments from employers into their Utoppia USD bank account.

From their USD balance, they can choose to convert to stablecoins and send payouts to any wallet globally, powered by BVNK. BVNK auto-converts USD to stablecoins and settles in minutes. This enables remote professionals, like a designer in Argentina working for US companies, to maintain their earnings in dollars while accessing and spending those funds globally.

Result:

- Near instant settlements: stablecoin payouts in seconds, not days.

- Stablecoin capabilities projected to grow Utoppia's annual revenue more than 40%.

- 50% of Utoppia's deposits projected to be in stablercoins within the year.

Demo: Global digital dollar accounts

Create an instant personalized demo, to see how your customers can create accounts and send or receive payments in stablecoins in your platform.

3. Global adoption

Key data-points to help you understand where demand is highest for stablecoin payment services.

Crypto ownership

Stablecoin ownership

Most popular stablecoins and networks

Stablecoin user demographics

Globally, stablecoin owners skews young, entrepreneurial. In BVNK’s 2026 Stablecoin utility report, which surveyed around 5000 users in 15 countries, we found:

- More than half of stablecoin owners and prospective acquirers are 18-34.

- 6 in 10 current/recent owners are men, but in middle- and lower-income economies, the gender split is more balanced.

- Those earning through business, entrepreneurship or active trading are more likely to own or show interest in stablecoins.

Where should you launch stablecoin wallets?

High opportunity markets show strong stablecoin adoption and fintech maturity and are well supported by infrastructure providers.

Medium opportunity markets have established but slower-growing adoption. Note that some markets are likely to be prohibited by your stablecoin infrastructure partner due to regulatory or risk restrictions. For a guide to high and medium opportunity markets, see below.

Note: This is based on BVNK’s assessment of both market adoption signals and fintech infrastructure maturity. It is provided for informational purposes only. It aims to give an indication of where stablecoin adoption is significant and where your services might gain traction. Market demand and availability of wallet infrastructure will also depend on your use case: speak to a BVNK expert for more guidance.

High opportunity markets

Argentina, Bangladesh, Brazil, Canada, Colombia, Egypt, Ethiopia, France, Germany, India, Indonesia, Japan, Jordan, Kenya, Mexico, Morocco, Nigeria, Pakistan, Philippines, South Africa, South Korea, Thailand, Turkey, Ukraine, United Kingdom, United States (all 50 states + DC + Puerto Rico), Venezuela, Vietnam, Yemen.

Medium opportunity markets

Algeria, American Samoa, Armenia, Australia, Austria, Belarus, Belgium, Bermuda, Bolivia, British Virgin Islands, Bulgaria, Cambodia, Cameroon, Cayman Islands, Chile, Croatia, Cyprus, Czech Republic, Denmark, Ecuador, Estonia, Falkland Islands, Finland, French, Polynesia, Georgia, Ghana, Gibraltar, Greece, Guam, Guatemala, Guernsey, Hong Kong, Hungary, Iraq, Isle of Man, Israel, Italy, Jersey, Kazakhstan, Kyrgyzstan, Latvia, Liechtenstein, Lithuania, Luxembourg, Malaysia ,Malta, Mann Island, Mariana Islands, Montserrat, Moldova, Nepal, Netherlands, New Caledonia, Norway, Paraguay, Peru, Poland ,Portugal, Romania, Saudi Arabia, Senegal, Serbia, Singapore, Slovakia, Slovenia, Spain, Sri Lanka, Sweden, Switzerland, Tanzania, Tunisia, Uganda, United Arab Emirates, Uzbekistan, Virgin Islands, U.S.

4. How wallets work: setup and responsibilities

Embedded stablecoin wallets enable businesses to offer stablecoin services to their customers under their own brand, in their own platform.

Who does what in an embedded model?

In an embedded model, your partner uses their digital asset license to deliver stablecoin services to your customers. They're responsible for processing payments, AML screening, KYC/B, and meeting regulatory standards set by their regulator.

Below we explain how this works operationally and legally (including compliance responsibilities, custody and onboarding process), using BVNK as the example provider.

Compliance FAQs

Does my business need to handle stablecoins?

There’s no need to handle stablecoins yourself if you prefer not to. In an embedded model, your provider delivers stablecoin services directly to your users through your platform. You leverage your provider’s digital asset licenses and they custody the stablecoins on behalf of your users.

How does custody of digital assets work?

In a custodial model, your customer’s stablecoin wallet is provided by your stablecoin partner and that provider securely holds and manages funds, handling compliance, (eg KYC and AML transaction monitoring) security, and operations.

In a self custody model, your user can create their own self-custodial stablecoin wallet in your app. They then control their own funds and private keys, and are responsible for their own funds. Your stablecoin partner may offer advanced recovery options for self-custodial wallets – for example, email-based recovery instead of relying solely on seed phrases.

It can be helpful to offer both custodial and self custodial options to your users – depending on local regulations, and user preferences. However it’s worth noting that self-custody wallets may be limited in their connectivity, since providers may not be able to offer regulated services such as conversion, through self custodial wallets.

How are funds safeguarded?

If your provider is keeping custody of digital assets on your behalf (ie they provide custodial wallets to your users), they should follow strict segregation practices to keep your digital assets safe.

Ensure your provider maintains a strict distinction between the treatment of fiat (traditional currency eg e-money ) and digital assets (stablecoins/crypto) to ensure compliance with relevant global regulatory standards. For example, under European payments and digital asset regulations, ‘Safeguarding’ refers to the regulation protection framework for e-money, while ‘Safekeeping’ is the name of the regulatory framework for digital assets in stablecoins. Your providers’ safeguarding and safekeeping practices should be subject to regular internal audits and external regulatory reporting to authorities.

For crypto assets, they must also maintain 1:1 asset backing and a full-reserve model (meaning they don’t engage in fractional banking, lending, or rehypothecation). Stablecoin payment providers should also keep an internal ledger – a real-time internal record of each client’s holdings and carry out daily reconciliation to cross-reference internal records with blockchain entries and bank statements to ensure our assets are always identifiable and 100% accurate.

Who manages compliance and AML?

Under an embedded model, your partner is using their digital asset license to deliver stablecoin services to your customers – they are responsible for processing payments, for AML screening, KYC/B, custody and meeting the standards set out by their digital asset licence.

Ensure your provider monitors transactions in real time using a combination of blockchain screening, sanctions screening, geolocation controls, and transaction monitoring rules. These controls are used to detect suspicious activity, identify exposure to prohibited or high-risk counterparties, and support AML investigation where needed.

At times, your provider may need to escalate or investigate transactions to meet regulatory requirements. Ask your provider about their process for this. For example, BVNK’s framework supports manual review and specialist escalation. This includes requests for information, deeper investigations, suspicious activity reporting where required, sanctions assessments, and local compliance oversight.

Who handles Travel Rule compliance?

The Crypto Travel Rule is a key piece of AML regulation for digital assets. It requires certain identifying information about the sender and recipient of digital asset transfers to be shared between cryptoasset service providers. It is now in force in many regions across the world. In an embedded model, your provider is responsible for Travel Rule compliance. This means they must collect and validate relevant sender and beneficiary information for applicable transactions, while preventing non-compliant transfers from being processed, in line with jurisdictional requirements. These requirements will impact certain parts of your user experience and operations – be sure to ask your provider what this means for you.

Who is responsible for customer support?

In most cases, you are still responsible for customer support and most businesses prefer to keep full control of direct communications with their own customers. It’s advisable to put in place SLAs with your provider to ensure their technical and support teams are on hand to quickly respond to and work with your support team, to resolve any issues that your customers face.

5. Product capabilities

A stablecoin wallet enables you or your users to store, send, receive and convert stablecoins. Additional products like cards and rewards can be layered on top.

Core functionality

Multi-currency balances

Embedded stablecoin wallets can hold balances in stablecoins or fiat currencies (eg USD, EUR, GBP). Regardless of which you hold, the wallet connects to both stablecoin and fiat payment rails. When payment currency differs from balance currency, auto-conversion typically occurs at the point of transaction.

Interoperable with fiat

Stablecoin wallets are typically connected to fiat payment rails like Swift, SEPA, ACH and Fedwire, enabling users to deposit and withdraw using relevant local and international payment rails.

Auto-conversion

Stablecoin wallets can support automatic conversion into your preferred settlement currency, whether stablecoin or fiat, at the point of receipt or payout. This is a technical capability to consider when evaluating infrastructure.

Supports multiple networks and tokens (no lock-in)

Different blockchains support different payment types – for example, Solana for micropayments. Users in different regions may prefer different stablecoins (USDT, USDC, PYUSD). Embedded wallets can support multiple networks (Binance Smartchain, Solana, Ethereum, Tron, Polygon) and multiple stablecoins.

Named accounts and payments

Under the hood, some embedded fiat wallets may use an omnibus or pooled account in your name. To make reconciliation easier, look for a provider that can issue segregated named virtual accounts in your customers’ names, for the currencies (and payment rails) you need.

Onboarding and support

User onboarding

The time it takes to onboard your users to stablecoin services has historically been a bottleneck across the industry, but this is changing, unlocking a step-change in time to launch. Eligible individuals can onboard to BVNK in minutes, and we’ve accelerated onboarding for businesses by 75% since 2025.

Launch support

Your embedded stablecoin partner should support you with:

- Go to market compliance:sharing real world examples on market adoption and use cases, and reviewing your user experience and marketing for adherence to relevant financial regulations.

- Team training:Ensuring your team staff understand the service and can handle stablecoin-specific questions from users if needed.

- Customer communication:providing examples of how to introduce stablecoin wallet features and educate customers.

- Monitoring adoption:reviewing usage and incentivization options for your users.

Ongoing customer support

It’s important you can resolve any issues quickly for your users, and that your provider enables you to deliver a high level of service. While your provider may not deal directly with your users, ensure you have SLAs in place with them for customer support. For example, BVNK’s average response time on support tickets is 3 minutes, with 24/7 support in place.

Value added services

Stablecoin cards

Users get a card linked to their stablecoin balance and can spend anywhere cards are accepted. For example, a remittance app user with an embedded stablecoin wallet sees an option to "Get a card" - they are issued a card by accepting some additional terms and in most cases, no additional information required. The user can view their card number, set/change pin within their app. They can add their card to Apple / Google pay. When they transact with this card, they see transactions pending/completed/ declined with merchant name, USD and local currency for the expense or charge.

Rewards

If your wallets provider has a rewards scheme in place, your users can earn on their stablecoin balances automatically, without locking up funds.

6. What to expect from wallets pricing

A guide to provider fees

The following are typical examples of fees you may incur with your stablecoin infrastructure partner.

Note: to discuss custom pricing for your needs, please reach out to the BVNK team.

Eg for a $5000 USDT transfer:Ethereum (ERC-20): ~$1-5Solana: ~$0.00025-0.001TRON (TRC-20):~$1-3 Bitcoin: ~$1-20

Some providers won't charge if the cost is very low. BVNK for example only charges for Ethereum, Bitcoin, and Tron.

Note: providers may not charge for deposits into their platform.

Higher spreads can decrease conversion on a pay-in, so find a provider that gives you flexibility on whether to apply this fee, or whether it's baked into your processing fees.

A guide to pricing your stablecoin service

Eg for a $5000 USDT transfer:Ethereum (ERC-20): ~$1-5Solana: ~$0.00025-0.001TRON (TRC-20):~$1-3 Bitcoin: ~$1-20

• No wallet fee during onboarding.

• Subsidized network fees on selected chains.

• Reduced or waived conversion spreads for initial transactions.

• Monthly active wallet fee (eg $1).

• Network fees passed through to end users.

• Volume-based discounts for larger customers.

7. Building your stablecoin experience

Your infrastructure partner should guide you through designing your user experience and helping you understand how to stay compliant.

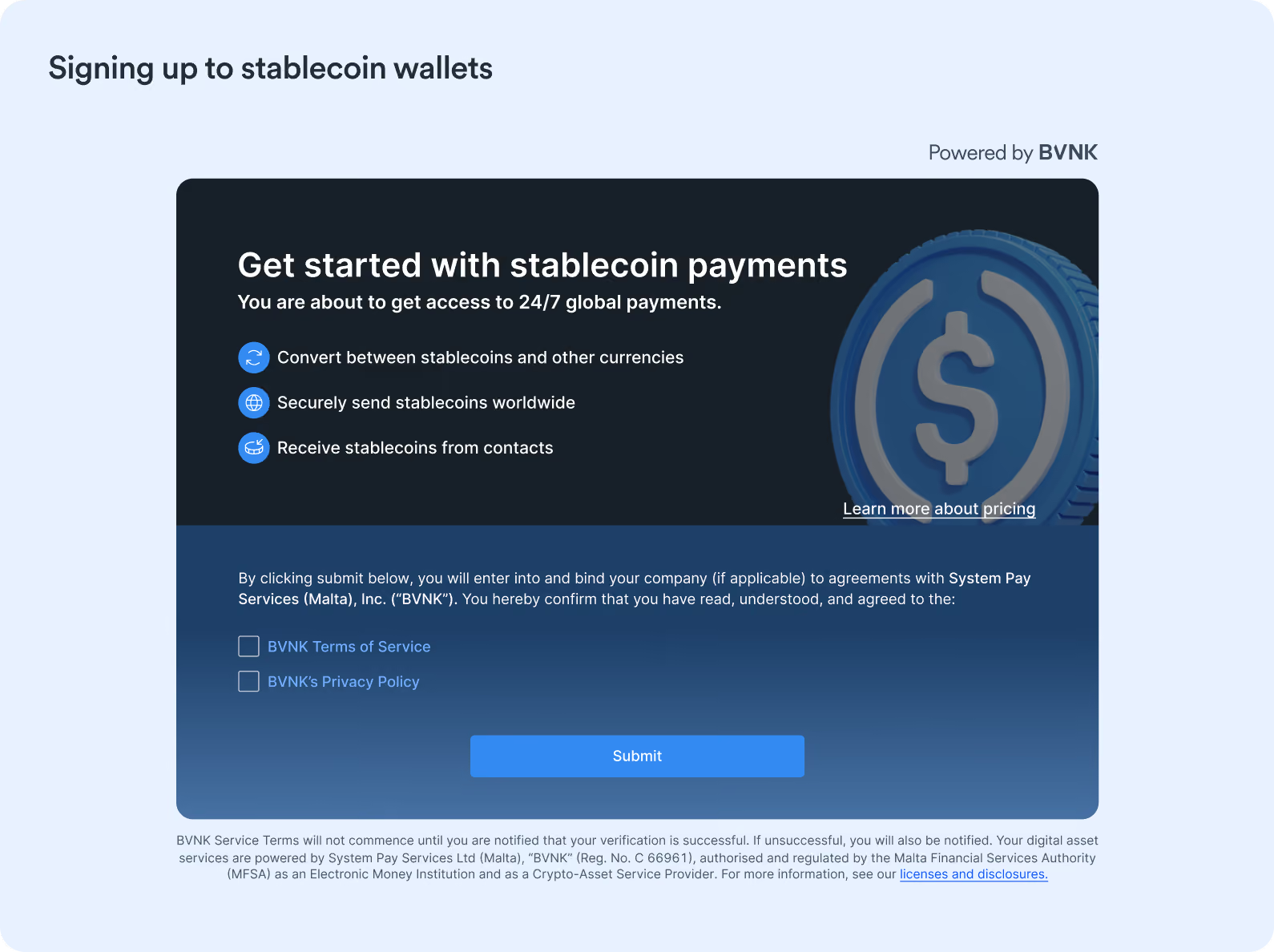

Creating your sign-up experience

Include key information on your sign-up page to ensure your users understand the service they are signing up to.

Before you start, ask your provider: How long does user review and verification take? How are applications approved/rejected? How should you communicate decisions and application status to users?

What information will you need to collect from your users?

You’ll need to give your embedded wallets provider certain information about your user to enable signup. This may change based on region and type of customer (ie business or individual), but is likely to include:

- Full name

- Email address

- Role (where applicable)

- Date and time they accepted BVNK’s service terms

- IP address when accepting BVNK’s service terms

You can ask your users to provide this when they sign up to the service, or pass it to your provider via API.

Learn more about the documents and information you’ll need to successfully onboard your customers to services powered by BVNK:

Designing your user journeys

Ask your provider for guidance on legal requirements and UX best practice for designing key user flows, including:

- Creating and naming their first wallet

- Adding recipients and senders

- Receiving stablecoins

- Sending stablecoins

- Confirming the payment

- Accessing account statements and transaction history

Below we share a few examples.

Launching your stablecoin service

Your stablecoin wallets partner should be there to support you with:

- Go to market strategy: sharing their expertise with you on markets and use cases, and reviewing your user experience and marketing for accuracy

- Team training: helping your team to understand the new service and handle stablecoin-specific questions from users if needed.

- Customer communication: sharing best practice examples on how to introduce benefits of stablecoin wallets (eg via homepage banners, emails, and in-app notifications) and educate customers (eg via FAQs, tutorials, and video explainers)

- User adoption: helping you evaluate usage and incentivization options for your users if needed.