Global stablecoin regulations 2026: What enterprises need to know

.avif)

Introduction

In 2026, stablecoins have entered the regulatory mainstream across seven major economies.

The US, EU, UK, Singapore, Hong Kong, UAE, and Japan now mandate full reserve backing, licensed issuers, and guaranteed redemption rights - treating stablecoins as regulated payment instruments rather than crypto assets.

For enterprises, this transformation provides the regulatory certainty needed to integrate stablecoins into payment infrastructure, but compliance now requires bank-grade systems supporting multi-jurisdictional operations.

This guide examines what each framework requires and how to adapt your payment stack.

Key takeaways

- Regulators are converging on common standards. Across major economies, stablecoin laws now require full reserve backing, clear redemption rights, and direct supervision of issuers.

- Stablecoins are moving into the payments mainstream. Frameworks such as the US GENIUS Act and the EU's MiCA bring stablecoins under the same prudential rules that govern banks and payment institutions.

- Compliance is an infrastructure challenge. You need systems that can support multiple regulatory regimes without slowing settlement speed or increasing risk.

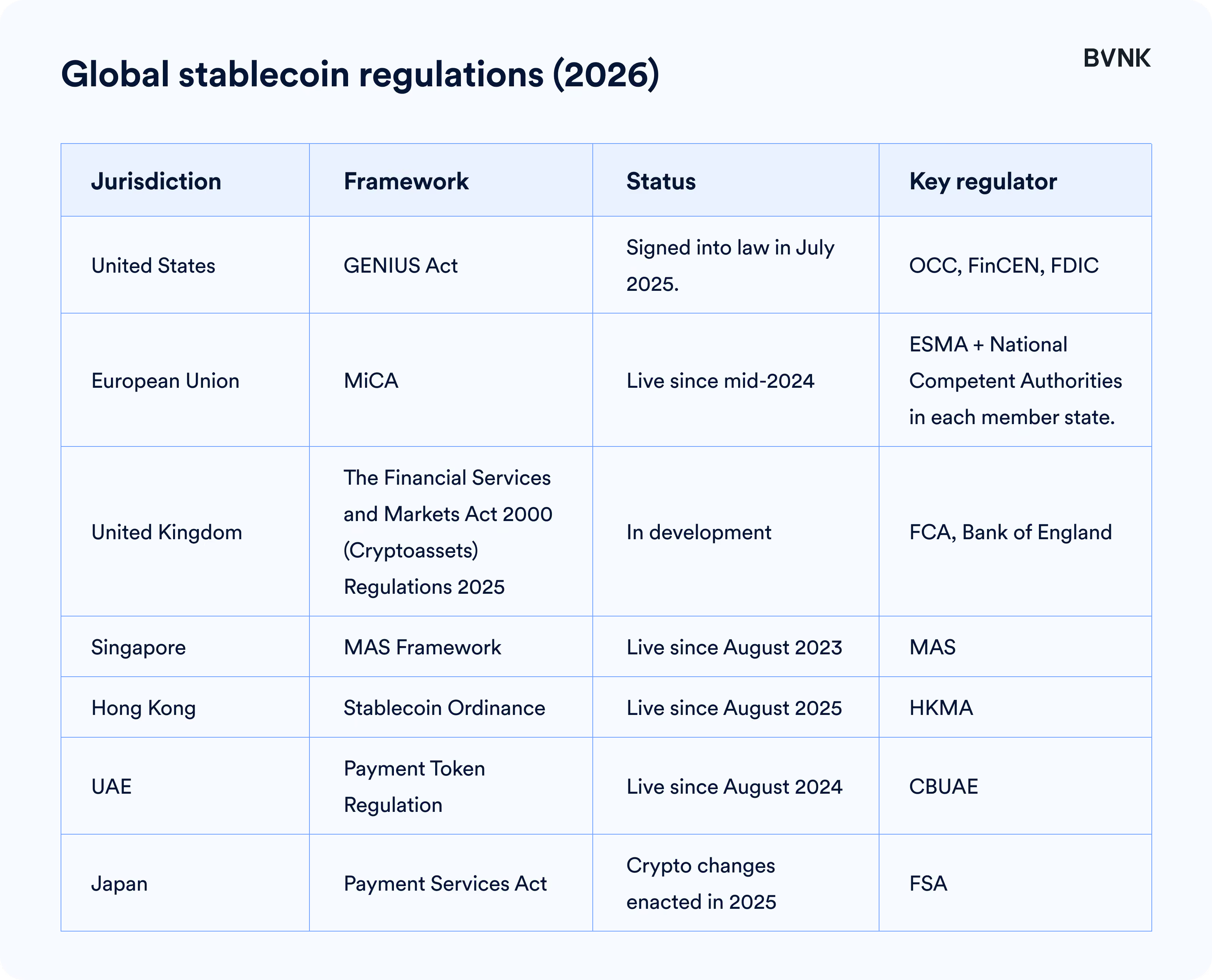

Quick comparison: Global stablecoin regulations (2026)

Why are stablecoins being regulated in 2026?

If your board or executive team has been asking whether stablecoins belong in your payment stack, you're not alone. In 2025, stablecoins have shifted from a niche crypto product to become a serious instrument for global payments.

You're likely already seeing the use cases: moving money faster across borders, reducing settlement risk, serving customers in multiple currencies around the clock. That enterprise demand has pushed regulators to act.

Across the world, governments see the same pattern: stablecoins can improve payment efficiency if they operate under the same standards that protect traditional finance.

Now, global regulators are setting clear rules for companies providing crypto services as well as those issuing stablecoins.

What are the major stablecoin regulations by jurisdiction?

1. United States: GENIUS Act stablecoin framework (signed into law 2025)

After years of uncertainty, the United States now has a federal framework for stablecoins.

The Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act, passed in July 2025, ends the patchwork of state-level licensing and agency overlap that defined US crypto policy for almost a decade.

The regulatory framework

The new law creates a clear definition of "payment stablecoins" and restricts issuance to regulated institutions. Banks, credit unions, and specially licensed non-bank issuers can now issue stablecoins under oversight from the Office of the Comptroller of the Currency (OCC).

The act explicitly classifies compliant stablecoins as neither securities nor commodities, which removes them from SEC and CFTC jurisdiction.

Key requirements:

- Payment stablecoin issuers under $10 billion can choose state-level regulation if that framework meets federal standards.

- Federally-regulated issuers can be either depository institutions or non-bank trusts approved by the OCC

- Payment stablecoins are not securities or commodities and are not FDIC-guaranteed.

- All approved issuers of payment stablecoins need to implement full audits, strict AML/KYC programs, and technology to freeze tokens when legally required.

- Payment stablecoins must have full backing with either fiat currency or high-quality liquid reserves in a 1:1 ratio.

- Issuers are prohibited from paying interest to stablecoin holders (though non-issuers like BVNK that custody such coins for their customers may offer “rewards” programs).

- 18-month implementation period until early 2027

2. United Kingdom: FCA stablecoin authorization requirements (effective 2026)

The United Kingdom is taking a phased, pragmatic approach to stablecoin regulation. The goal: bring digital settlement assets into the financial mainstream while preserving stability and consumer protection.

The regulatory framework

The foundation was set in the Financial Services and Markets Act (FSMA) 2023, which formally recognized fiat-backed stablecoins used for payments as part of the UK's regulated perimeter.

Now, HM Treasury, the Bank of England, and the Financial Conduct Authority (FCA) are developing detailed rules for stablecoins focused on fiat-referenced stablecoins used for payments.

Any business issuing or holding these assets in the UK will need FCA authorization, including overseas issuers whose tokens circulate within UK payment systems.

Key requirements likely to include:

- Full reserve backing in liquid assets

- Redemption guaranteed at par value

- Customer funds segregated from operating funds

- No interest on stablecoin balances

- Compliance with existing payments and e-money rules

- Bank of England oversight for systemically important stablecoins

Secondary legislation is expected to take effect during 2026.

3. European Union: MiCA stablecoin regulation (live since mid-2024)

The European Union has taken the lead in turning stablecoin policy into law. The Markets in Crypto-Assets (MiCA) framework, adopted in 2023 and live since mid-2024, gives Europe the world's first unified rulebook for digital assets.

The regulatory framework

MiCA draws a sharp line between two token types:

- Electronic Money Tokens (EMTs): Backed one-to-one by a single fiat currency

- Asset-Referenced Tokens (ARTs): Link to baskets of assets such as multiple currencies or commodities

Algorithmic tokens don't qualify as "stable" at all – a deliberate move to avoid the unbacked models that fueled earlier market failures.

Key requirements:

- Only EU-authorized credit and e-money institutions can issue EMTs/ARTs

- Issuers must be EU-incorporated

- Published white paper approved by national regulators

- 100% backing by high-quality, liquid assets

- Reserves held with reputable custodians in same currency as token

- Redemption guaranteed at par value

- No interest on holdings

- European Banking Authority (EBA) oversight for significant-scale tokens

- Limits on non-euro stablecoin usage for payments to protect euro stability

4. Singapore: MAS stablecoin framework (live since 2023)

Singapore has built one of the most detailed and conservative stablecoin frameworks in the world. The Monetary Authority of Singapore (MAS) finalized its rules in August 2023 after several years of consultation.

The regulatory framework

The framework applies to single-currency stablecoins pegged to the Singapore dollar or G10 currencies (US dollar, euro, yen, etc.). Issuers that meet all MAS requirements can label their tokens as "MAS-regulated stablecoins" – a label that signals prudential standards equivalent to traditional financial instruments.

Key requirements:

- One-to-one reserve backing in same currency

- Reserves in high-quality liquid assets (cash or short-term sovereign debt)

- Reserves segregated and held with licensed custodians

- Monthly attestations and annual audits

- Redemption at par value within five business days

- Minimum base capital and liquidity reserves

- Prohibition on other crypto trading or lending activities

- Strong balance sheet requirements

5. Hong Kong: HKMA stablecoin licensing regime (live since 2025)

Hong Kong has moved quickly to build a clear, enforceable framework for stablecoins. The Stablecoin Ordinance, passed in May 2025, established a mandatory licensing regime overseen by the Hong Kong Monetary Authority (HKMA).

The regulatory framework

The law focuses on fiat-referenced stablecoins – tokens that maintain a stable value relative to one or more national currencies. Algorithmic or crypto-collateralized stablecoins are excluded.

Any company that issues, markets, or distributes fiat-backed stablecoins to the public in Hong Kong must hold an HKMA license. This includes foreign issuers offering Hong Kong dollar-pegged tokens.

The framework took effect in August 2025 and provides a sandbox for firms to test stablecoin operations under supervision before seeking full authorization.

Key requirements:

- Local incorporation required

- Minimum paid-up capital of HK$25 million (unless already a regulated bank)

- One-to-one backing by high-quality, liquid reserve assets in segregated accounts

- Redemption at face value without delay or excessive fees

- No yield or interest on balances

- Strict risk management, cybersecurity, and disclosure requirements

- Regular audits and ongoing reporting to HKMA

- Distribution entities must be approved as "Permitted Offerors"

6. United Arab Emirates: CBUAE payment token regulation (live since 2024)

The United Arab Emirates has taken a layered but coordinated approach to stablecoin regulation, building an integrated framework that connects federal oversight with regional innovation.

The regulatory framework

At the federal level, the Central Bank of the UAE (CBUAE) regulates fiat-backed stablecoins under its Payment Token Services Regulation, effective from August 2024. This regulation defines "payment tokens" as crypto assets fully backed by one or more fiat currencies and used for settlement or transfers.

Any company that issues, redeems, or facilitates payment tokens in the UAE mainland must hold a Central Bank license.

Outside the mainland, several regional regulators (VARA in Dubai, SCA, FSRA in Abu Dhabi Global Market, DFSA in Dubai International Financial Centre) have aligned their standards with the federal framework.

Key requirements:

- One-to-one reserve backing

- Customer assets segregated from operating funds

- Strict governance and transparency standards

- The first licensed stablecoin, AE Coin, launched under this framework in late 2024, pegged to the dirham

The UAE treats stablecoins as part of financial infrastructure supporting payments, remittances, and trade, while balancing private-sector innovation with its own central bank digital currency rollout (the Digital Dirham).

7. Japan: Payment Services Act stablecoin rules (live since mid-2023)

Japan was one of the first countries to bring stablecoins under a formal legal regime. In June 2022, Japan's parliament amended the Payment Services Act to define and regulate "digital money-type stablecoins." The law came into force in mid-2023.

The regulatory framework

The law creates a clear distinction:

- Digital money-type stablecoins: Fiat-pegged assets redeemable at face value

- All other price-stable tokens: Including algorithmic and crypto-collateralized coins, which fall under existing crypto asset rules and can't be marketed as stablecoins

Only licensed financial institutions can issue stablecoins in Japan: banks, registered fund transfer service providers, and trust companies. Banks can issue stablecoins as deposit-like instruments with the highest level of consumer protection.

Distribution is also tightly controlled – any platform facilitating buying, selling, or custody must register with the Financial Services Agency (FSA).

Key requirements:

- Full reserves in cash or highly secure assets

- Reserves segregated from issuer's own funds

- Strict AML and cybersecurity standards

- Consumer redress mechanisms

- Asset segregation requirements

- Prohibition on lending/trading activities for issuers

The first wave of domestic stablecoins, including JPYC and Progmat Coin, began launching in 2024, many backed by major Japanese financial institutions.

Common principles across stablecoin regulations

Governments worldwide are drawing stablecoins into the core of the financial system, setting consistent expectations for reserve quality, redemption rights, and issuer accountability.

Across jurisdictions, the message is clear: stablecoins are no longer operating in a legal vacuum.

Despite regional differences, the new frameworks share several common principles:

- Only licensed and supervised entities can process and issue stablecoins

- Reserves must be fully backed and easily redeemable

- Holders should have the same protections as users of other regulated payment instruments

Each jurisdiction is adapting these ideas to its own financial structure, but the direction of travel is unmistakable – it's heading towards convergence.

What enterprises need to know

This shift changes how you need to think about payments infrastructure. Stablecoins are moving from an experimental technology to a reliable settlement layer that can connect markets in real time. New regulation is creating the conditions for large-scale adoption among enterprises and fintechs.

The challenge now lies in operational alignment. Operating across jurisdictions requires working with partners who have global licensing, robust automated compliance controls, and the foresight to guide you through an evolving regulatory landscape.

As rules align across markets, the advantage will belong to businesses that can move quickly while staying compliant.

The frameworks covered in this article represent the foundation, not the finish line. Expect continued evolution as regulators refine their approaches, add cross-border coordination mechanisms, and integrate stablecoins with central bank digital currencies. The core principles are now established, and implementation details will continue to evolve.

FAQs

What are the main global stablecoin regulations in 2026?

The main global stablecoin regulations in 2025 are the U.S. GENIUS Act, EU MiCA, Singapore's MAS framework, Hong Kong's Stablecoin Ordinance, UAE's Payment Token Regulation, and Japan's Payment Services Act. Each defines how stablecoins must be issued, backed, managed and supervised in their respective jurisdictions.

What principles are common across all jurisdictions?

The principles common across all jurisdictions are mandatory licensing for service providers and issuers under financial supervision, mandated AML and KYC screening and controls, issuers to keep 1:1 fiat reserve backing, redemption at par value for holders. These core principles drive convergence toward treating stablecoins as regulated payment instruments.

How does MiCA differ from the US GENIUS Act?

MiCA differs from the U.S. GENIUS Act in that MiCA provides a unified EU-wide rulebook covering crypto assets, while the GENIUS Act focuses specifically on payment stablecoins.

Are algorithmic stablecoins regulated?

Algorithmic stablecoins are not regulated under most major frameworks. Most jurisdictions exclude them because they lack full reserve backing, and they cannot be marketed as "stablecoins" under MiCA, GENIUS Act, or Singapore's framework.

Why is stablecoin regulation considered beneficial for enterprises?

Stablecoin regulation is considered beneficial for enterprises because it provides predictability and legal clarity, which businesses need to integrate stablecoins into mainstream payment systems. Clear frameworks enable partnerships with regulated financial institutions and reduce operational risk.

How can businesses comply with multiple jurisdictions simultaneously?

Businesses can comply with multiple jurisdictions simultaneously by partnering with global stablecoin providers that hold licenses across key markets, maintain automated compliance infrastructure, and actively monitor regulatory developments to keep you ahead of changes.

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

Never miss an insight.